Related Articles

.png)

Jan 08, 2025

Jan 08, 2025

Is Varicose Vein surgery covered under the health insurance policy in India

Health Insurance

Health Insurance

.png)

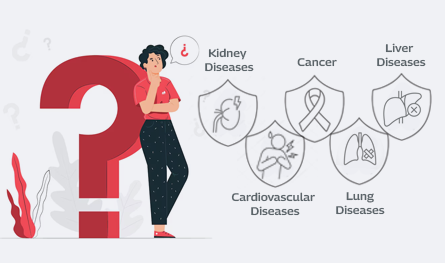

Critical illness insurance is an exclusive medical cover that offers financial protection to the insured individual for treating certain listed critical ailments. Usually, critical illness plans are fixed-benefit health insurance plans. It is a type of health insurance policy that provides a lump sum payout if the insured person is diagnosed with any of the listed critical illnesses specified in the policy document, such as cancer, heart attack, kidney failure, or stroke, irrespective of the amount spent in hospitalisation.

The list of critical illnesses that the chosen plan will cover remains mentioned in the policy documents. This is usually an over-the-counter plan with no pre-medical check-up but with a declaration of good health. It is a comprehensive plan that can be easily acquired and is available in individual and family floater plans.

Critical illness insurance is beneficial for:

Critical illness insurance varies slightly from standard health insurance plans.

This type of plan offers a fixed lump sum benefit to the insured individual on the diagnosis of any of the listed critical ailments or undergoing any specific treatment. Once this payment is complete, the coverage for that ailment automatically ceases. You can utilise the payout to continue with the treatment processes.

Thus, the insurer pays the entire lump sum insured upon diagnosis of a covered critical illness, regardless of the actual medical expenses incurred.

The plan covers a predefined list of critical illnesses mentioned in the policy document, wherein the sum insured is paid on diagnosis alone, irrespective of the mode of treatment.

The payout is not linked to medical bills or hospital expenses. You can use the amount as needed, such as for treatment, recovery, physiotherapy, loss of pay or even household expenses.

Standalone critical illness plans are pretty reasonable and do not burden your pocket. You can use the premium calculator to assess the probable premium payable amount based on your circumstances and proceed accordingly.

Most plans have a waiting period from the policy inception date, during which claims cannot be made.

Some policies require the insured to survive for about 30 days after diagnosis to claim the benefit. Thus, standalone critical illness plans are referred to as Survival Benefit Plans.

Thus, standalone critical illness plans can be taken along with indemnity health insurance plans. The indemnity plan can pay for the hospitalisation expenses, while the lump sum payout can be utilised for any other expenses.

When compared to standard health insurance plans, critical illness policies offer certain typical benefits:

When you opt for a high sum insured amount under critical illness insurance, you ensure comprehensive coverage for yourself and your family. This is especially helpful for treating critical ailments, which often involve complex and expensive medical procedures. If you’re diagnosed with any critical illnesses your insurer lists, you’ll receive a lump sum payout to cover treatment expenses. The payout frequency depends on the terms of your chosen plan, giving you timely financial support when you need it most.

Critical illness insurance covers a variety of severe health conditions, such as cardiovascular diseases, cancer, kidney failure, coma, and more. However, the list of covered illnesses varies by plan and insurer. Review the policy details carefully to ensure it meets your needs and avoids unexpected financial strain.

You can also add critical illness coverage as a rider to your existing health insurance policy. This enhances your basic health plan, giving you extra financial security. Even if you already have a standard health policy, a critical illness rider ensures you’re better prepared to handle the financial impact of severe illnesses.

If you’re diagnosed with a critical illness, it might prevent you from working, potentially disrupting your family’s financial stability. With critical illness insurance, the lump sum payout can help cover treatment costs and replace lost income, ensuring your family’s financial needs are met during challenging times.

Critical illness insurance plans are available at reasonable premium rates, making them accessible to many individuals. If you have pre-existing diseases (PEDs) or are at risk of critical illnesses, securing a CI policy ensures peace of mind and financial stability. Combining health insurance with critical illness coverage further enhances your protection.

The premiums you pay for critical illness insurance are eligible for tax deductions under Section 80D of the Income Tax Act. You can claim up to Rs 25,000; if you’re a senior citizen, the limit increases to Rs. 50,000 under the Old Tax Regime. This makes it a financially smart choice for you and your family.

In summary, critical illness insurance provides essential financial support, covers various ailments, and offers affordable protection with added tax benefits. It’s a valuable addition to your financial planning in India, ensuring you’re prepared for life’s uncertainties.

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 17 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Jan 08, 2025

Health Insurance

.png)

When you sign up for a life insurance policy - whether it’s a traditional term insurance policy or a ULIP – you are not just buying peace of mind. You are also trusting the insurer with your money. So naturally, you would want to know: How is that money being managed? And more importantly, how is it being protected from risky decisions?

Have you ever caught yourself lost in illusions about your daughter's future events, such as her university convocation and first day at work? Her university convocation. When she embarks upon her initial job after graduation will be the day.

Term insurance is an important investment. However, with the availability of so many insurers offering term plans, it becomes difficult to select the best term plan to suit your needs. Buying a term plan needs some consideration and research on the part of the policyholder. In this post, let us discuss the best term insurance providers in India.

In a country where medical inflation is rising rapidly, securing a comprehensive health coverage plan for the entire family is no longer optional, it is essential. Selecting the right health insurance requires careful evaluation of multiple factors, not just premium costs. A well-chosen plan ensures financial security, access to quality healthcare, and peace of mind during medical emergencies.

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.

.png)