Understanding Riders in Term Insurance: Which Ones To Choose?

Life is unpredictable. The effects of a loss of life in a family not only affect the demised person, but the family members also suffer tremendous emotional and financial crunches, especially when the demised was the principal breadwinner.

Considering such unpredictability, the insurance companies have launched term life plans. This is essentially a life cover plan, exclusively crafted to sustain the family members after the policyholder’s demise.

The coverage is offered for a pre-defined period in exchange for a pre-determined premium already paid. The beneficiaries receive the death benefit if the policyholder passes away during the plan tenure. However, if the policyholder and the insured individual are different and the insured person passes away, the insurer provides no benefit.

This is a pure life coverage plan, i.e., it does not offer any investment or savings benefit. If the insured outlives the plan tenure, then also he/she will receive any benefit from this.

However, you can enhance the protection span by adding befitting riders to the base plan.

What are term insurance riders?

This is a typical optional benefit that the insured individual can avail of to make the base plan more comprehensive. A term insurance rider is an additional add-on which optimises the overall benefits of the base plan. This gets activated only after a specific event has occurred.

The term insurance rider benefits are absolutely optional. It aids in customising the principal plan up to a certain extent.

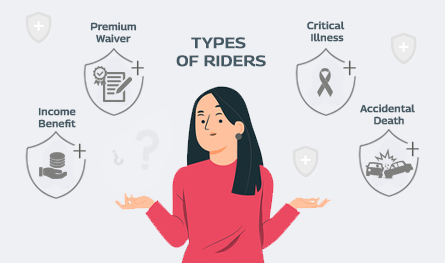

List of common riders in term insurance

The overall coverage span of term life can be extended according to your convenience by adding add-ons to the basic plan. Some of the popular term insurance riders include the following:

1. Accidental Death Rider:

Observing the increasing number of accidents, it has become almost imperative to ensure protection against such unforeseen circumstances. A standard term plan offers death benefits, but in an accidental death scenario, this rider enhances the insurance coverage. So, by choosing this rider, the family members of the concerned policyholder receive accidental death benefits apart from the sum assured protection of the base plan.

2. Critical Illness Rider:

This rider has been specifically crafted to allow coverage on detection of any listed critical ailment like cancer, cardiovascular diseases, cardiac arrest, coma, etc. Treating such issues can obliterate your savings fast. So, attaching this rider to your base plan can save you from such rainy days. You will receive a lump sum benefit from your insurer on diagnosis of any of the listed critical ailments as followed by your insurer. Moreover, it also acts as an income substitute as you become unfit to work due to your ailment.

3. Permanent and partial disability rider:

This rider has been designed to cover the loss of temporary or permanent disability caused by an accident. This proves to be essentially helpful during such tough times as it copes with both the high treatment costs and income loss. Depending on the level of disability, either the sum assured or a percentage of it is paid to the insured. However, several insurers often waive future premium dues under such circumstances without plan discontinuation.

4. Premium waiver rider:

With this rider, your future premium dues get waived, keeping your plan active, especially during accidents or disabilities leading to income loss. Depending on the terms of your chosen plan, the death benefit is also offered. This rider helps you to retain your peace of mind despite challenging unprecedented circumstances.

5. Accelerated death benefit rider:

This has been crafted to cover losses caused by terminal ailments like leukaemia, cancer, etc. Under this rider, the insurer usually offers 50% of the amount of the sum assured on detection of any listed terminal ailment while the remaining 50% is paid as a death benefit to the nominee after the demise of the insured.

6. Income benefit rider:

If you go by the name, you can understand that the term insurance rider acts as a way of income substitution during any unfortunate event. This proves to be a saviour, especially if the insured person happens to be the sole breadwinner in the family. It happens to efficiently manage the financial distress caused due to such unfortunate events.

Author Bio

Paybima Team

Paybima is an Indian insurance aggregator on a mission to make insurance simple for people. Paybima is the Digital arm of the already established and trusted Mahindra Insurance Brokers Ltd., a reputed name in the insurance broking industry with 17 years of experience. Paybima promises you the easy-to-access online platform to buy insurance policies, and also extend their unrelented assistance with all your policy related queries and services.

Other Life Insurance Products

Latest Post

Taxpayers should know more about Section 139(1) of the Income tax act since it is the section under which they have to file their returns if they have missed filing within the due date.

Have you ever caught yourself lost in illusions about your daughter's future events, such as her university convocation and first day at work? Her university convocation. When she embarks upon her initial job after graduation will be the day.

In a country where medical inflation is rising rapidly, securing a comprehensive health coverage plan for the entire family is no longer optional, it is essential. Selecting the right health insurance requires careful evaluation of multiple factors, not just premium costs. A well-chosen plan ensures financial security, access to quality healthcare, and peace of mind during medical emergencies.

Term insurance is an important investment. However, with the availability of so many insurers offering term plans, it becomes difficult to select the best term plan to suit your needs. Buying a term plan needs some consideration and research on the part of the policyholder. In this post, let us discuss the best term insurance providers in India.

.png)

When you sign up for a life insurance policy - whether it’s a traditional term insurance policy or a ULIP – you are not just buying peace of mind. You are also trusting the insurer with your money. So naturally, you would want to know: How is that money being managed? And more importantly, how is it being protected from risky decisions?

Speak to our Advisor

+91

By clicking the button, I authorize Paybima advisor to contact me via SMS, Email, Phone, WhatsApp or any other modes overriding my 'DND'.T&C Apply.